Article published in ERJ’s March/April issue:

London - Tire companies are preparing for some challenging months ahead as the cost of raw materials is expected to increase through the course of the year.

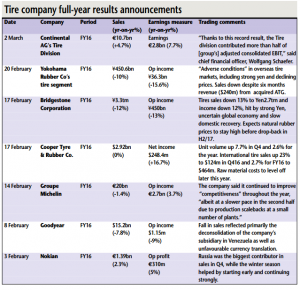

As the annual results season approached, tire companies almost unanimously agreed that cost pressure which soared in the final quarter of 2016 was likely to stay for 2017, prompting global price rises for products.

While Michelin saw a 1.4% decline in sales to €20 billion, operating income rose 3.7% to €2.7 billion. This, it said, was due to higher volumes and a rebound in demand in China.

In 2017, however, Michelin expects tire markets to track the trends observed in late 2016, in particular with an upturn in mining tire sales.

“The year will also see an increase in raw materials costs, for an estimated impact of approximately €900 million,” said Michelin.

In response to the cost pressure, Michelin said it will “agilely manage prices so as to hold unit margins firm in businesses not subject to indexation clauses.”

German automotive supplier Continental AG also saw growth in its Tire Division, with sales up 4.7% at €10.7 billion and earnings 7.7% higher at €2.8 billion. This, said Conti, was due to “record number of tires sold throughout 2016.”

For 2017, the German group expects raw material costs to have a negative impact of €500 million on its results. This contrasts with the €150-million positive impact of lower raw materials prices noted in 2016.

A pick-up in Russia and the early and steady winter season helped Finnish tire maker Nokian register a “strong performance” in the final quarter of 2016. Mostly thanks to its passenger car tire business unit, which covered 65% of the total group sales, Nokian’s full year results showed a 2.3% growth in sales to €1.39 billion and nearly 5% rise in operating profit to €310 million.

The world’s biggest tire company Bridgestone, however, struggled along with other Japanese tire makers due to a strong yen, the uncertain global economy and slow domestic recovery.

Bridgestone’s sales fell 12% to ¥3.3 trillion for the full year 2016, while operating income declined 13% to ¥450 billion.

Similarly, Yokohama Rubber cited “adverse conditions” in overseas tire markets, including strong yen and declining prices for a -10% fall in sales to ¥450.6 billion, despite the addition of six months’ revenue of ¥25.5 billion from acquired ATG.

Yokohama’s tires segment posted a 15.6% drop in operating income to ¥36.3 billion.

In the US, Goodyear suffered a 7.8% fall in sales to $15.2 billion, due in part to the deconsolidation of its subsidiary in Venezuela and a strong dollar. Segment operating income declined 2% to $2 billion. Volumes totalled 166.1 million, essentially unchanged from the year before.

Cooper Tire, on the other hand, saw net income improve 16% to $249 million on flat sales of $2.9 billion. According to Cooper, slow demand in the US was offset by double-digit volume and sales rises in Europe and China.

Elsewhere, in China, the tire & rubber products sector reported a €141 billion revenue in 2016, at a growth rate of 2.6% compared with 2.1% in 2015.

According to information released at the 2017 China Rubber Conference held in Guangzhou mid-March, the sector’s profit rose by 6% to €8.8 billion, compared with a 3% drop in 2015, while investment in the sector increased 8% to €25 billion.