Article published in May/June issue of ERJ

London - After five years of steep decline, some green shoots of recovery are beginning to emerge in the natural rubber market. But opinion is divided over whether these shoots will be strong enough to survive.

ERJ’s snapshot of prices at the end of March showed that prices for RU1609, the most heavily traded rubber future on the Shanghai Futures Exchange, reached Yuan 11,370/tonne, almost 13-percent higher than in the first week of trading this January. In Japan, meanwhile, rubber prices closed at Yen167.0/kg on the TOCOM exchange, about 14 percent above the levels of early January.

Even bigger increases were recorded between early January and the end of March on rubber exchanges in Thailand and Malaysia.

Temporary recovery

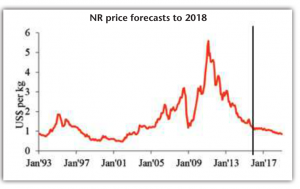

Daily NR prices recovered sharply towards the end of February and early March, agreed Dr Prachaya Jumpasut, market analyst and publisher of the Rubber Economist. But, he believes that “these improvements are only temporary as the long-term problem of the large amount of surplus and production capacity will still be there in the next few years.”

Trading in March, suggested Jumpasut, might have been influenced by the start of the wintering season in southeast Asian countries as well as the announcement of agreed export cuts by the members of the International Tripartite Rubber Council (ITRC).

Under the ITRC agreement, Thailand, Indonesia and Malaysia plan to withdraw exports of 615,000 tonnes of NR for six months, from 1 March to 31 Aug 2016, while also increasing domestic consumption.

But such export controls need to be applied along with production control, said Jumpasut, noting that the Thai government also plans to purchase around 200,000 tonnes of local rubber at a price 50-percent above the current market rate. Moreover, he said, export controls are very difficult to manage, as OPEC has often demonstrated.

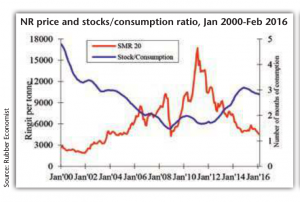

Despite recent decreases, the global NR stocks/consumption ratio has remained stubbornly high: its rate of decline has been marginal given the huge level of global stocks, he said.

On the other hand, suppliers point out that low natural rubber prices, caused by factors including oil prices, lower demand than forecast and a weak global equity market, may lead to a slowdown in new planting.

In a speech at the 2016 China Rubber Conference in Qingdao, China, Sheela Thomas, secretary general of the Association of Natural Rubber Producing Countries (ANRPC) warned that “the reported large [natural rubber] stock overhang is only on paper.”

Last year, global natural rubber production dropped slightly to 11.8 million tonnes, lower than global consumption pegged at 11.9 million tonnes. “Farmers find it very hard to justify production,” she said. “They are looking to the government for solutions.”

Thomas also pointed to the potential impacts of changes in China, which accounts for 40 percent of global natural rubber consumption, and imports 80 percent of what it consumes: “Its various economic situations and rubber policies, such as the depreciation of yuan and the new tariff policy on compound rubber that curbs imports, hold strong influence over the global industry.”

China takes up half of Thailand’s natural rubber export, and “I don’t expect the percentage to change any time soon,” said the Thai Rubber Association’s deputy secretary general Paitoon Wongsasutthikul at the Qingdao conference.

Procurement schemes

Additionally, Thailand initiated above-market-price procurement of 100,000 tonnes of rubber sheets, and India has announced a scheme that subsidises smallholders with the difference between the current price and the government’s fixed price.

“Such measures have not led to any long-standing impact on price,” Thomas insisted.

Jumpasut at the Rubber Economist, though, believes that overall “the fundamentals still look grim for NR prices to be on a steady increasing trend during the next few years.

“Our forecast points to NR prices remaining weak until demand picks up to absorb the large amount of global stocks,” he commented.

“However, there should not be a sharp decline as experienced earlier, but a stable or a gradual decline.”