Akron, Ohio – For the first time in several years, the US tire industry held its own and even clawed back a bit of market share from imports, according to information gleaned from the pages of the 2016 Market Data Book - published in the 15 Feb edition of ERJ sister publication Tire Business.

US tire manufacturers increased their output across the board last year, according to the latest Rubber Manufacturers Association (RMA) data, posting gains of 4.2, 1.4 and 2.1 percent in passenger, light truck and medium truck/bus tire production, respectively.

For the first time in years, US production growth outdistanced import growth in the car and light truck sectors. US truck/bus tire production growth fell short of the 9.3-percent gain in imports, however, when the RMA and Department of Commerce data are compared.

Production of passenger tires rose to 126.1 million units, light truck tires to 26.4 million units and medium truck tires to 14.8 million units, the RMA data show. The combined total of 167.8 million units was the highest since 2011.

By contrast, imports of passenger and medium truck tires rose 0.4 and 9.3 percent, respectively, to 149.5 million and 14.4 million units. Imports of light truck tires slipped 6.4 percent to 24.3 million units.

Imports of passenger tires from China – the object of the US’s elevated import duties – fell 53.2 percent from record levels in 2014, but overall imports were up slightly as South Korea, Thailand, Indonesia and Taiwan all registered double-digit increases over 2014 to compensate for the drop in Chinese shipments.

US tire makers also boosted their exports last year across the board, shipping 2.1-percent more passenger tires, 2.7-percent more light truck tires and 5.4-percent more medium truck tires to export markets, the RMA data show.

Exports represented roughly 20 percent of car and light truck tire production and 16 percent of medium truck/bus tire output. Canada and Mexico represented roughly 80 percent of US car tire exports, two-thirds of light truck tire exports and more than 90 percent of truck/bus tire exports.

Bridgestone also is considered a leader on the retail of the ledger, reporting an estimated $4.5 billion in sales through its Bridgestone Retail unit, slightly ahead of mega retailer Discount Tire/America’s Tire.

Discount Tire operated 910 stores are year-end 2015, compared with the 2,313 stores under Bridgestone’s control.

Other nuggets gleaned from the Market Data Book include:

Demand for high-performance tires in the U.S. continued to increase, especially on the replacement side, where tires H rated and higher now represent 38.2 percent of aftermarket shipments. Growth on the OE side, which had averaged 40 percent the past five years, plateaued a bit last year, while still accounting for more than half of OE fitments. Shipments of aftermarket speed-rated tires rose 10.2 percent to 78.7 million units, while those to OE customers were up 4 percent to 25 million units.

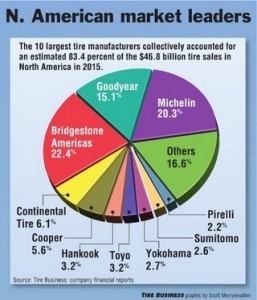

Goodyear remained the No. 1 supplier of OE consumer tires last year, outfitting an estimated 28 percent of the 17.7 million cars, SUVs and light trucks built in North America in 2013 with its Goodyear and Dunlop brands. Michelin North America. was No. 2 with its Michelin and BFGoodrich brands, ahead of Bridgestone Americas (Bridgestone and Firestone brands) and Continental Tire the Americas LLC (Continental and General brands).

The roster of OE suppliers will grow to an even dozen this year when Sumitomo Rubber USA LLC starts supplying its Falken brand to a few select vehicles.

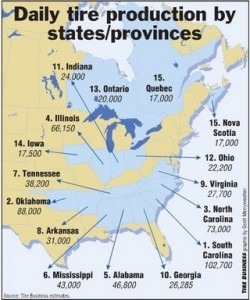

South Carolina’s status as the No. 1 tire-producing state grew, with estimated daily tire production growing to nearly 103,000 units as expansions by Bridgestone Americas, Continental Tire and Michelin started having an effect. Two more plants — those of Trelleborg Wheel Systems (opened in January 2016) and Giti Tire Group (due on stream in 2017) will expand that total even more in coming years.

Import brands claimed more than a quarter of the U.S. passenger and light truck replacement markets, while the domestic makers’ flag and associate brands represented more than 60 percent of each category, according to Tire Business’ analysis of RMA and Commerce Department data.

US shipments of winter/traction tires grew slightly to a 3.6-percent market share, up from 3.5 percent in 2013. By contrast, winter tires represent 35 percent of aftermarket car tire shipments in Canada. Ironically, unit shipments are roughly 7 million in each country.

The Market Data Book also contains benchmarking information on the automotive service sector and summaries of Tire Business’ retail, commercial and retread rankings from 2015.