Article originally published in the Nov/Dec edition of European Rubber Journal magazine:

London - This year has seen a marked business-slowdown in the French rubber industry, following a 2017 resurgence across the country’s tire and industrial rubber products sectors, SNCP (Syndicat National du Caoutchouc et des Polymères) has reported.

While production volumes across both product types grew by just 1% last year, this nevertheless represented a significant improvement on previous years, according to the national industry association.

Indeed, it said, growth figures for sales, exports, margins and investment were probably the best recorded for the rubber industry for many years.

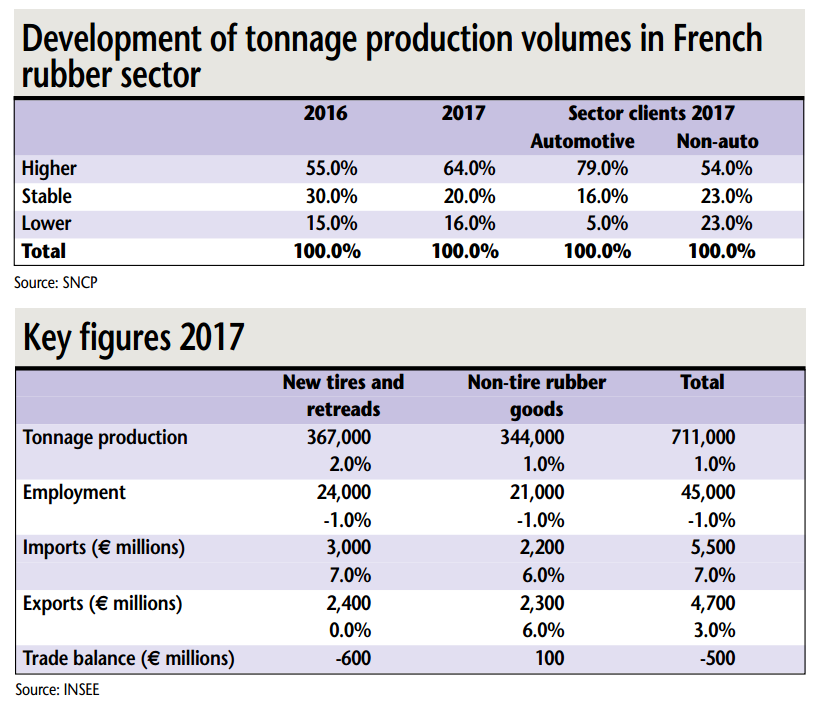

For 2017, 64% of industrial rubber companies reported an increase in production volumes; up from just 55% the year before. A similar improvement was reported in terms of sales last year.

Likewise, at the start of 2018, early two third of businesses reported growth in both volumes and pricing. Such positivity, said SNCP, has not been seen since 2011 as the industry rebounded from the global financial crisis.

Since early 2018, however, the business situation for French manufacturers has reversed, so that by the end of June rubber-parts production volumes were just about on a par with prior-year levels.

Automotive growth

In terms of market sectors, automotive rubber suppliers continue to deliver the highest growth and, in 2018, look certain to outperform those supplying other markets for a fifth straight year.

Margins in the rubber processing industry also remained at high levels during 2017, according to the association.

Average net profitability in the industrial rubber sector stayed above 4% for the fourth year in a row. Rising raw materials prices are, however, likely to impact earnings in the current year.

There was, though, some disparity in business performance, SNCP noted. While 50% of companies improved net margins in 2017, another 24% saw a deterioration – compared to only 12% reporting lower profits in 2016.

During 2018, supply issues returned to the market for rubber raw materials for the first time in four years. This followed months of cool-down in the market from a spike in butadiene and natural rubber prices early last year.

The association also noted that, current market pressures have impacted prices for some, rather than most rubber materials – as has been the norm in the past.

Last year’s mini-crisis, however, left its mark: the proportion of rubber processors reporting significant increases in materials costs reaching 50 % – compared to around 17% in 2016.

Such tensions have continued during 2018, though for particular material types, including nitrile rubber, polychloroprène and carbon black.

The trend has been driven by an increasing disparity between production capacities and fast-growing demand and the impact of rising crude oil prices on certain materials.

On the other hand, prices for natural rubber have continued to decline, due particularly to oversupply and a slowdown in Chinese demand, said SNCP.

The number of people working in the French tire and industrial rubber goods manufacturing sector fell by just under 1% in 2017, to around 45,000 – continuing a prior-year recovery in employment levels.

Despite the industry’s buoyancy last year, some of the increased activity was absorbed by productivity gains linked to new equipment, automation and the use of temporary workers.

In 2017, the proportion of companies that increased their workforce was close to a 10-year-high of 40% in the industrial rubber sector, SNCP also pointed out.