Based on feature article published in ERJ’s May/June issue

Carbon black demand rising but faces pressure from all sides in the tire fillers market, numbers presented by Paul Ita of Notch Consulting show:

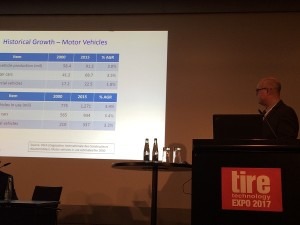

Growth in the market for tire fillers is closely linked to levels of vehicle production, tire production, rubber consumption, reinforcing-filler demand and crude oil prices, according to Paul Ita, president of Notch Consulting Inc. of Amherst, Massachusetts.

Vehicle production has grown at a rate of 3% over the last 15 years and reached 91.2 million units in 2015 – driven by passenger cars with 3.5% growth and commercial vehicles at 1.8%.

In terms of vehicles in use, the growth rate was 3.4% with about 1.3 billion vehicles in use globally, Ita added in a presentation at the TTE conference in Hanover earlier this year.

The trend is similar for the tire and rubber segment, though with slightly stronger growth for passenger car tires versus truck & bus tires.

On the rubber-demand side, Notch predicts growth of 2.8% to nearly 27 million tonnes, while tire production is estimated to reach 2.6 billion units by 2030, of which 2 billion units will be passenger car tires.

In terms of growth, the tire industry’s total consumption of compounding ingredients – not including tire cord – will rise from about 29 million tonnes in 2015 to 46 million tonnes in 2030, Ita forecast.

Looking more closely at the reinforcement fillers segment, Notch estimates that the market will grow from about 10 million tonnes in 2015 to 15 million tonnes in 2030.

This, said Ita, will include an increased share for silica from about 9% to 13% – continuing a trend seen over the last 10 years.

While carbon black is the product most under threat from silica, the Notch expert said “not all segments are under equal threats by any stretch.”

A 2015 analysis of the 9 million tonnes of carbon black used in tires, showed that the most exposed segment was passenger car tread, which accounts for about 15% of all carbon black consumed in the tire market.

“That is where most of the substitution has taken place up until now,“ said Ita.

However, the Notch president went on to identify some threats also in the truck & bus tread segment with the emergence of technologies that overcome the problems of mixing silica with natural rubber.

This issue has limited use of silica in the truck & bus tires, but with some suppliers now making the filler more compatible with natural rubber, Ita expects “a slight threat” to carbon black in this market.

But the main challenge to carbon black is in the passenger car tire segment, with silica set to reach about 15% penetration, up from about 10% in 2015 – equating to around 800 kilotonnes (kt) less demand for carbon black.

An overriding factor in this is the price of crude oil: increased oil and raw materials prices will make tires companies much more likely to substitute fossil fuel-based materials.

Ita also examined factors that could disrupt the tire fillers market, among them tire weights, extended mobility systems, oil-free tires and alternative fillers such as recovered carbon black.

A particularly tricky question, he said, concerned tire weights, which are being driven up as major tire-makers strive to counter competition in lower-priced tires by focusing on large-diameter tires.

“It seems that every tire expansion that I read about these days is either building a new plant for large-diameter tires or converting an existing small-tire capacity... to large-diameter tires,” said Ita, who sees this trend continuing.

On the other hand, electric vehicles are increasing demand for smaller tires, as is the popularity of city and micro cars which also tend to use smaller tires.

Weight reduction

Airless tire designs and the greater use of solution styrene butadiene rubber to produce thinner sidewalls and inner liners are also helping reduce tire weights. So even if tires remain the same size they can still be lighter through the use of less materials.

Ita also analysed the impact of extended mobility systems and the trend to get rid of full-size spare tires on the tire filler market.

Between 2000 and 2015, he estimated that elimination of spare tires has led to a reduction of about 19 million car tires – equivalent to about 91 kt of rubber, 48kt of carbon black and 6kt of precipitated silica.

Projecting that forward to 2030, Ita estimated that there will be around 12 million cars without spare tires. This would mean a demand-reduction of about 58kt of rubber, 30kt of carbon black and 4kt of precipitated silica.

In the emerging area of airless tires, Ita said Michelin’s Tweel had become a “pretty significant” product, with other companies working on these products, including Bridgestone, Sumitomo and Hankook. Current applications, however, are limited mainly to low-speed vehicles without suspensions.

“If these tires come into commercial applications, the implications for reinforcing fillers will be pretty serious,” said Ita, noting that they need 50% less carbon black and 33% less silica than a conventional pneumatic tire.

The Notch leader went on to discuss the prospects for a range of other alternative fillers, including recycled carbon black (see below) graphene, precipitated silica and products derived from natural and/or waste feedstock.

The key issues for all potential replacement materials, he said, will be longevity, treadwear, cost, implications for mixing and other processes, performance and commercial availability.

“Ultimately we are talking about oil prices,” Ita concluded. “Will oil prices will be high enough for the tire companies to progressively look into alternative materials, particularly for synthetic rubber and carbon black which are very oil-dependent.”