Article from the annual ERJ China Tire Report 2016, published as a supplement in the July/August issue of European Rubber Journal magazine:

While heavy import tariffs and countervailing duties imposed by the US and economic slowdown have impacted Chinese tire makers hard, the industry still plans to up its game in both domestic and overseas markets.

China’s tire industry is, for instance, moving to raise quality and brand value, through measures ranging from the introduction of labelling regulations to the promotion of technological advances, such as automation and Industry 4.0.

And despite all the current pressures on the industry, China expects tire production to total a fairly healthy 572 million units for 2016, according to Mary Xu, secretary general of the China Rubber Industry Association (CRIA).

Of this output, truck tire output will have negative growth of 3.6 percent down to 106 million units, while car tire production will rise by 2.9 percent to 417 million, Xu said at the ERJ-sponsored Future Tire Conference, 24-25 May in Essen, Germany.

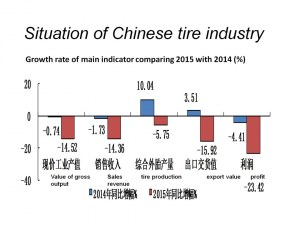

As Xu put it, the Chinese tire industry had its “worst year” in 2015 with many factories suffering losses and exports declining considerably.

CRIA’s tire data – based on the 40 major companies it surveyed – shows that total sales dropped by 15.4 percent to €18.2 billion with total profit down by 22.2 percent to €880 million.

In terms of sector-wide production volume, CRIA’s figures for its member companies suggest a 0.5-percent rise to 565 million units in 2015.

Meanwhile Chinese government data, which covers the entire industry, suggests a 4-percent drop to 925 million units last year.

According to CRIA, a 13-percent growth in the value of exports from China’s tire sector in 2014, was followed by a nearly 16-percent drop, to €12 billion last year.

The decline in sales led to the closure of a number of tire making plants last year, including units operated by Shandong Deruibo Tire in February, Capital Tire in March and Giti Chongqing in November.

In addition to that, a number of smaller tire makers, including Chuanghua Tire in Rizhao, Shandong and Fulltour in Linyi, Shandong were shut down last year with bigger names posting overall losses.

Also, the acquisition of two smaller companies in Shandong province, HengYu and Huaqiao, respectively by Doublestar and Hengfeng, added further to suggestions that the industry is entering a period of consolidation.

Indeed, Chinese officials have signalled a trend towards assets reorganisation of state-backed companies and policies that would favour the development of larger and stronger tire manufacturers.

According to Xu, the Chinese government has an aggressive plan to cut 40 percent of production by 2020 – mainly by beefing up its regulation of the industry.

New regulations, she said, will place tougher requirements, particularly on smaller companies and new entrants, in terms of emissions, energy efficiency and the environmental impact of tires being produced.

In late 2014, the government introduced “market access conditions” for the tire industry with new regulations regarding environmental protection.

Commenting on the conditions at the time, Zhu Hong, head of CRIA’s technological and economic committee said “a majority of smaller companies with high energy- and material- consumption will find it rather difficult to comply.”

The tightened environmental regulations, according Xu, can be a helpful lever in the drive to consolidate the industry which is now shifting its focus from quantity to quality.

Xu also told ERJ that she expected that the Chinese tire industry would become more focused on “tire technology innovation and tire branding.”

Anti-dumping duties

The main current driver for change in the Chinese tire industry is the imposition of anti-dumping tariffs and countervailing duties by the US against imports of passenger car ties from China.

The tariffs almost halved China’s passenger car tire exports to the US last year in both volume and value terms, to 314,000 tonnes and $874 million, said Xu.

Truck and bus tire exports from China to the US, meanwhile, decreased by 10 percent in volume, to 590,000 tonnes, and 21 percent in value, to $1.5 billion.

“The ratio of passenger car tire exports to the US overall dropped from 29 percent in 2014 to 18 percent last year, and the same thing is likely to happen to truck and bus tires in light of the ongoing anti-dumping probe,” said Xu.

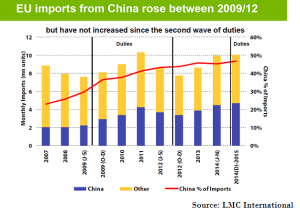

In Europe, there’s been a rise in imports of Chinese truck and bus tires.

This has impacted particularly the retreading sector in Europe, with the proportion of retreads falling to less than 24 percent of the replacement market for medium-to-heavy truck tires sales in 2015.

According to Gerard Stapleton, head of South East Asian research at market research company LMC, truck tire imports to the EU reached “record levels in 2015, passing the previous highest level in 2007,” with “all of the growth basically from China.”

The trend has sparked serious debates about lack of legislation and regulatory enforcement in the EU to stop cheap, low-quality tires being imported, and the European Commission has been urged by local retreaders to investigate the issue.

Exports to EU

But since the US imposed anti-dumping and countervailing duties in late 2014, the Chinese industry has increased in focus on Europe as an export destination for tires.

With a quarter of exports destined for Europe, the region has become China’s second largest PCR tire target market.

The European market is “very important for Chinese car tire manufacturers,” said Xu, who listed the UK, Germany, The Netherlands and Spain among China’s top 10 export destinations.

Of the import volume, the UK takes in the lion’s share with 38 percent, followed by Germany with a 15-percent share. Italy, Belgium and France are also among the key European destinations for Chinese passenger car tires.

“These eight countries alone account for 24 percent of the Chinese total tire exports,” Xu pointed out.

LMC’s Stapleton confirmed this growing appetite for exporting to the EU following the tariffs introduced by the US.

EU light vehicle tire imports, he noted, peaked in 2011 – when a previous round of US tariffs diverted Chinese tires to the EU – and the region is nearly back up to that level now.

“Since 2011, we saw a decline in imports, coinciding with the introduction of tire labelling [by the EU]. Now we are almost back up to that level again,” said the analyst adding that most of the tires are imported from China.

Look to the future

Despite the hits, there are bright spots within the industry, most outstanding of which stem from the state-owned ChemChina and its aggressive acquisition policies.

In the past few months, ChemChina has completed its €7-billion purchase of Italian tire giant Pirelli.

For now, ChemChina’s tire companies are working under the umbrella company China National Tire & Rubber Co.

Another development to watch is the overseas expansion of larger Chinese companies – particularly to southeast Asian countries, such as Vietnam and Thailand, which offer cheap labour and raw materials.

There are signs of further expansion outside the region with ChemChina-owned Beijing Research & Design Institute of Rubber Industry planning to build Bangladesh’s “first tire plant” by 2018.

Also, Qingdao Sentury Tire has announced plans to invest several hundred million dollars in a passenger car tire plant in the US, with 2017 as the target for the project.